News & Insights > Should you be considering selling your company to an Employee Ownership Trust (‘EOT’)?

Should you be considering selling your company to an Employee Ownership Trust (‘EOT’)?

24.05.23

Share

The EOT is a fast-growing and attractive business model. Research conducted by the Employee Ownership Association suggests that, as at December 2022, there were around 1,300 employee-owned businesses operating in the UK. Factors such as business owners wanting to exit since the COVID-19 pandemic and the long-mooted possibility of a rise in capital gains tax (‘CGT’), could go some way to explaining this trend.

EOTs have a number of benefits: for example, the transactions tend to be quicker and smoother (with lower transaction costs), they can be used to engage and drive employees to grow the company and they allow shareholders to sell the controlling interest free from CGT.

We look at the structure, benefits and disadvantages of the EOT model in further detail, below.

What is an EOT?

An EOT is a particular type of employee benefit trust which enables a company to become owned by its employees (i.e. a ‘John Lewis’ model). EOTs can be set up by existing owners of a company or be used as part of an exit or succession planning strategy. As well as a number of attractive tax incentives, the sale of a company to an EOT also has many other practical benefits, as explored further below.

How does a sale of a company to an EOT work?

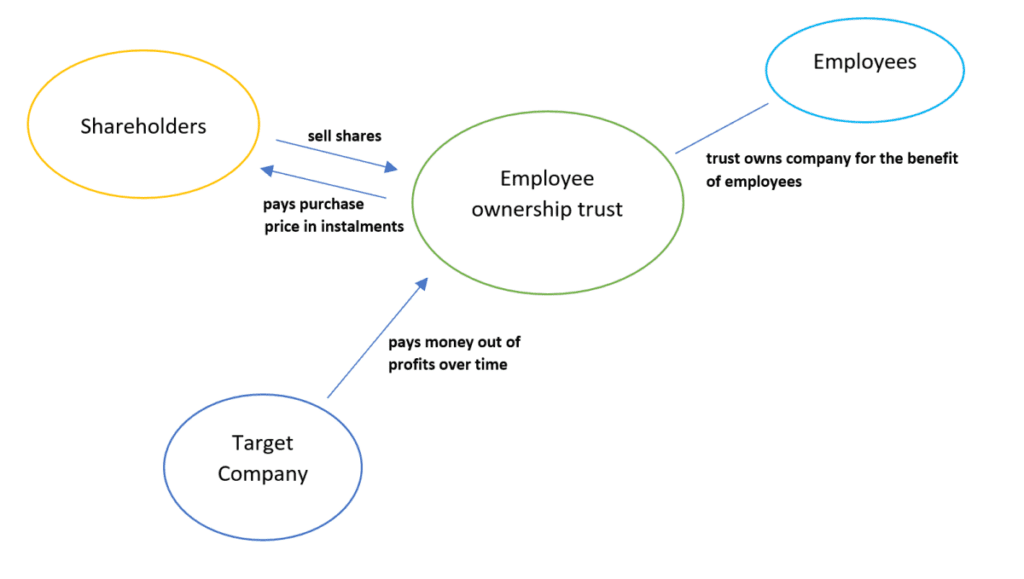

The sale of the company (Target) usually comprises three key stages:

Establish the EOT: A qualifying EOT will be established with a corporate trustee (Trustee Company).

Sale of shares in Target: under a share purchase agreement, the Target’s shareholders (Shareholders) sell their shares in the Target to the Trustee Company under a share purchase agreement. This process requires an external valuation of the Target’s shares to be agreed with HMRC and this valuation informs the purchase price. The purchase price is not paid in full on completion, but at least part of it is left outstanding as a debt owed by the Trustee Company to the Shareholders (see diagram below).

Gradual payment of purchase price: as the Target generates trading profits each year, these profits are paid to the EOT, usually by way of dividends. The Trustees use these profits to pay back the outstanding purchase price to the selling shareholders.

Diagram:

What are the advantages of a sale to an EOT?

Tax

The sale of a controlling interest in the company is entirely free from capital gains tax.

Bonuses paid to an employee of a company owned by an EOT are exempt from income tax (but not national insurance) up to £3,600 per employee per year.

The sale of shares to the EOT will not give rise to any inheritance tax issues provided that the legislation is followed.

Other

For exiting shareholders, this is generally a friendlier and cheaper alternative to a trade sale, MBO or liquidation.

No need for earn-outs which may not become payable in the future.

Employees who are well acquainted with the business are locked in for the future – this stimulates employee engagement and commitment for the long term.

No personal investment is required from the employees.

Enables preservation of the business, its culture and values and provides comfort that the legacy of the owners will endure.

Directors and management team of the target business can remain in place and focus on running the company as opposed to spending time and resources on more protracted sale negotiations (for example to a trade buyer or under an MBO).

Are there strings attached?

Yes. The legislative conditions to be satisfied in order for a sale to an EOT to qualify for the desired tax advantages are quite stringent. The key conditions are as follows:

The target company must be carrying on a trade (or alternatively be the principal company of a trading group).

The trustees of the EOT may only apply the trust property (the shares in the target company) for the benefit of all eligible employees on the same terms (and although this applies, for example, to bonuses, bonus amounts can be varied by reference to factors such as salary and length of service).

The trustees must at all times hold a controlling interest in the target company.

There are restrictions on the number of persons who remain shareholders after the sale to the EOT and who are also employees or directors of the target company.

Although it is primarily aimed at companies, it is also possible for businesses being run as limited liability partnerships and groups to put in place employee ownership structures using an EOT. Businesses at the start of their journey can also be established with an EOT in place where there is a desire on the part of the owners to secure maximum commitment and engagement and pursue a common path.

It is also possible to combine an EOT structure with a management incentive for key individuals after the sale; such as an EMI share option plan for the key employees running the company.

So, if you are considering a sale or an internal reorganisation of your business which can benefit both you and your employees, an EOT could be an attractive option.

Our corporate and corporate tax team are experienced in dealing with EOT structures. To speak to us about whether an EOT is right for you and should you have any other questions, please do not hesitate to contact Anthony Reeves.